The Future of Fair Lending: From 1071 to Algorithmic Accountability

Fair lending compliance has always been one of the most consequential areas of the regulatory examination cycle. Violations carry legal, reputational, operational, and enforcement risks that few other compliance findings can match.

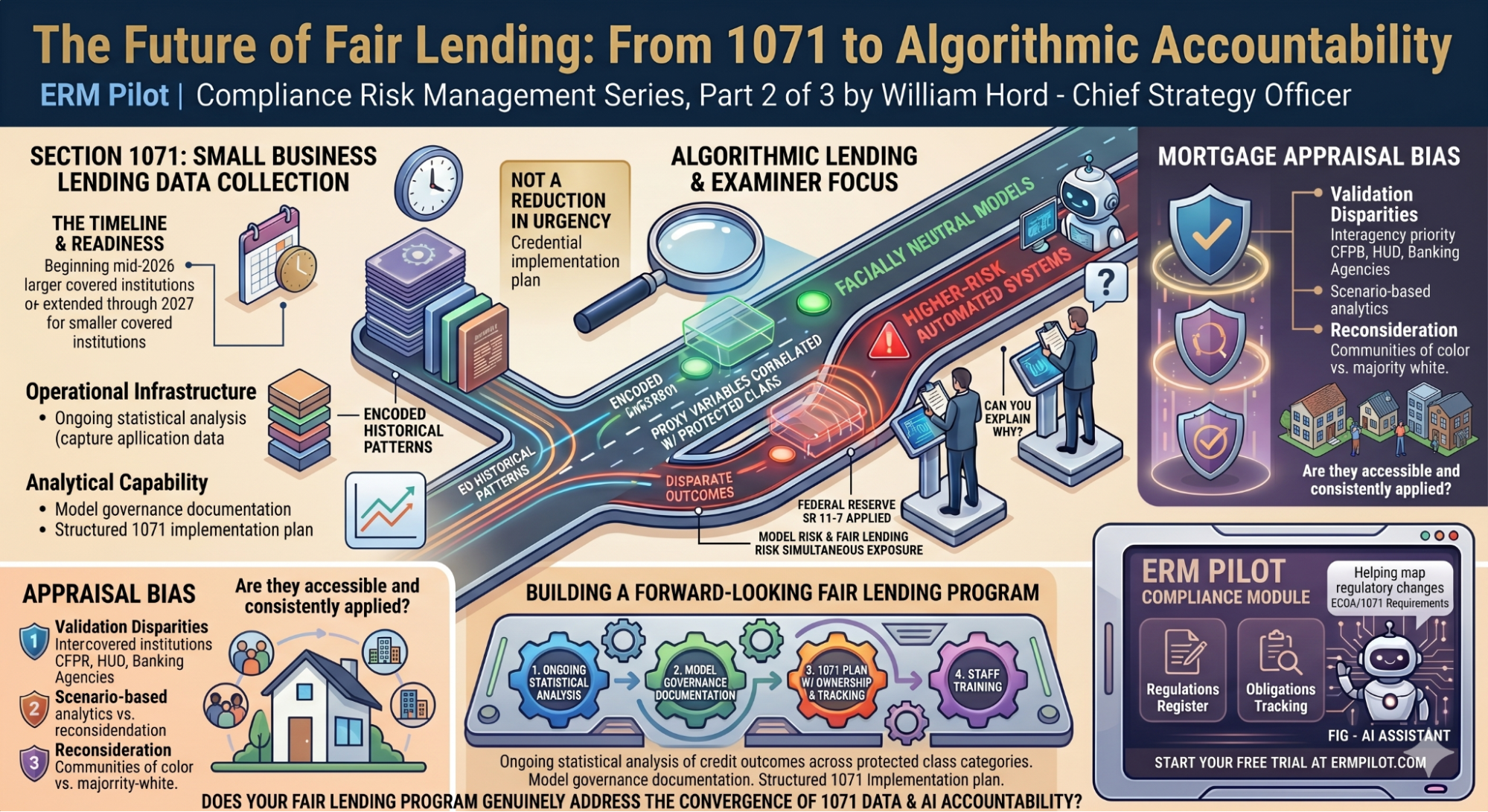

As institutions move through 2026, fair lending programs are increasingly being shaped by three interconnected developments: evolving Section 1071 requirements, growing use of automated and AI-assisted lending processes, and heightened scrutiny of valuation practices and appraisal bias.

The common theme is straightforward: regulators are placing greater emphasis on data, transparency, and governance.

Section 1071 Is Driving Long-Term Compliance Planning

The CFPB's Section 1071 rule implements the small-business lending data collection requirements established under the Equal Credit Opportunity Act.

Although implementation timelines have shifted multiple times through litigation, rule revisions, and compliance extensions, the underlying expectation remains unchanged: covered institutions will eventually need the capability to collect, validate, analyze, and report extensive small-business lending data.

The operational challenge extends far beyond regulatory reporting.

Institutions must build systems capable of capturing required demographic and application data, establish data quality controls, train staff on collection procedures, and develop analytical capabilities that allow management to identify potential fair lending concerns before regulators review the data.

Rather than focusing solely on future compliance deadlines, institutions should focus on building sustainable governance and data management processes that can support eventual implementation regardless of future rule adjustments.

Automated Lending Does Not Reduce Fair Lending Responsibility

As financial institutions increasingly incorporate automated decision systems, machine learning models, and AI-assisted underwriting tools into lending processes, regulators have made clear that fair lending obligations remain unchanged.

Whether a credit decision is made by a loan officer, a traditional scoring model, or an advanced algorithm, institutions remain responsible for ensuring that lending outcomes comply with fair lending laws.

The central regulatory concern is that automated systems may unintentionally produce discriminatory outcomes through historical data patterns, model design choices, or variables that serve as proxies for protected characteristics.

As a result, examiners are increasingly focused on whether institutions can demonstrate appropriate oversight of automated lending systems, including:

- Model governance and documentation;

- Independent validation and testing;

- Fair lending analysis of lending outcomes;

- Change management controls;

- Ongoing monitoring for disparate treatment and disparate impact risks; and

- Management understanding of how automated decisions are generated.

The question is no longer whether institutions use automation. The question is whether they can govern it effectively.

Model Risk Management and Fair Lending Are Converging

Many institutions continue to rely on SR 11-7 as the foundational framework for governing credit models and automated decision systems.

While originally developed as model risk management guidance, its core principles—including model inventory management, validation, performance monitoring, documentation, and independent review—have become increasingly important as institutions deploy more sophisticated automated underwriting tools.

This creates a growing intersection between model risk management and fair lending compliance.

Institutions that cannot adequately validate, monitor, or explain automated lending systems may face supervisory concerns related to both model governance and fair lending risk.

Appraisal Bias Remains a Significant Regulatory Focus

Federal banking agencies, the CFPB, HUD, and other federal stakeholders continue to emphasize concerns surrounding appraisal bias and valuation equity.

Regulators are increasingly focused on whether institutions have processes in place to identify potential valuation disparities, respond appropriately to borrower concerns, and maintain effective reconsideration-of-value procedures.

Examiners may evaluate:

- Policies governing appraisal reviews;

- Reconsideration-of-value processes;

- Escalation and complaint management procedures;

- Monitoring for potential valuation disparities; and

- Oversight of third-party appraisal providers.

Institutions should expect appraisal-related controls to remain an important component of fair lending examinations.

Governance Is Becoming the Defining Fair Lending Theme

Perhaps the most significant shift occurring across fair lending examinations is the growing emphasis on governance.

Regulators increasingly want evidence that institutions can identify emerging risks, evaluate the impact of regulatory developments, govern automated decision systems, and implement effective controls before problems emerge.

Strong fair lending programs increasingly include:

- Ongoing statistical analysis of lending outcomes;

- Governance frameworks for automated decision systems;

- Formal model validation processes;

- Structured Section 1071 implementation planning;

- Board and management reporting; and

- Targeted training for employees involved in lending, model oversight, and compliance functions.

Looking Ahead

The future of fair lending compliance will be defined less by manual file reviews and more by data governance, analytical capability, and oversight of increasingly complex lending technologies.

Institutions that establish strong governance frameworks today will be better positioned to navigate evolving Section 1071 requirements, manage automated lending risks, and meet examiner expectations in the years ahead.

Article References — The Future of Fair Lending: From 1071 to Algorithmic Accountability

1. Consumer Financial Protection Bureau. Small Business Lending under the Equal Credit Opportunity Act (Regulation B) — Section 1071 Final Rule. Washington, D.C.: CFPB, March 30, 2023; amended May 1, 2026 (compliance date extended to January 1, 2028). Available at:https://www.consumerfinance.gov/1071-rule/

2. Consumer Financial Protection Bureau. 'Small Business Lending Collection and Reporting Requirements.' CFPB Compliance Resources. Available at:https://www.consumerfinance.gov/compliance/compliance-resources/small-business-lending-resources/small-business-lending-collection-and-reporting-requirements/

3. Board of Governors of the Federal Reserve System. SR 26-2: Revised Guidance on Model Risk Management. Washington, D.C.: Federal Reserve, April 17, 2026. (Supersedes SR 11-7, April 4, 2011.) Available at:https://www.federalreserve.gov/supervisionreg/srletters/SR2602.htm

4. Office of the Comptroller of the Currency. Fiscal Year 2025 Bank Supervision Operating Plan. Washington, D.C.: OCC, October 2024. Available at:https://www.occ.gov/news-issuances/news-releases/2024/nr-occ-2024-111a.pdf